Current as at 26 June 2026

As the 2026 financial year comes to a close, Australian taxpayers, employers and small business owners should be aware of selected tax and superannuation developments that may affect year-end planning, payroll processes and compliance obligations.

This article summarises selected tax and superannuation developments that may be relevant to Australian taxpayers and businesses around 30 June 2026. It is not a complete summary of all tax changes and should not be relied on as tax advice. The correct tax treatment will depend on each taxpayer’s specific facts, residency status, income profile, business structure, documentation, timing and applicable legislative requirements.

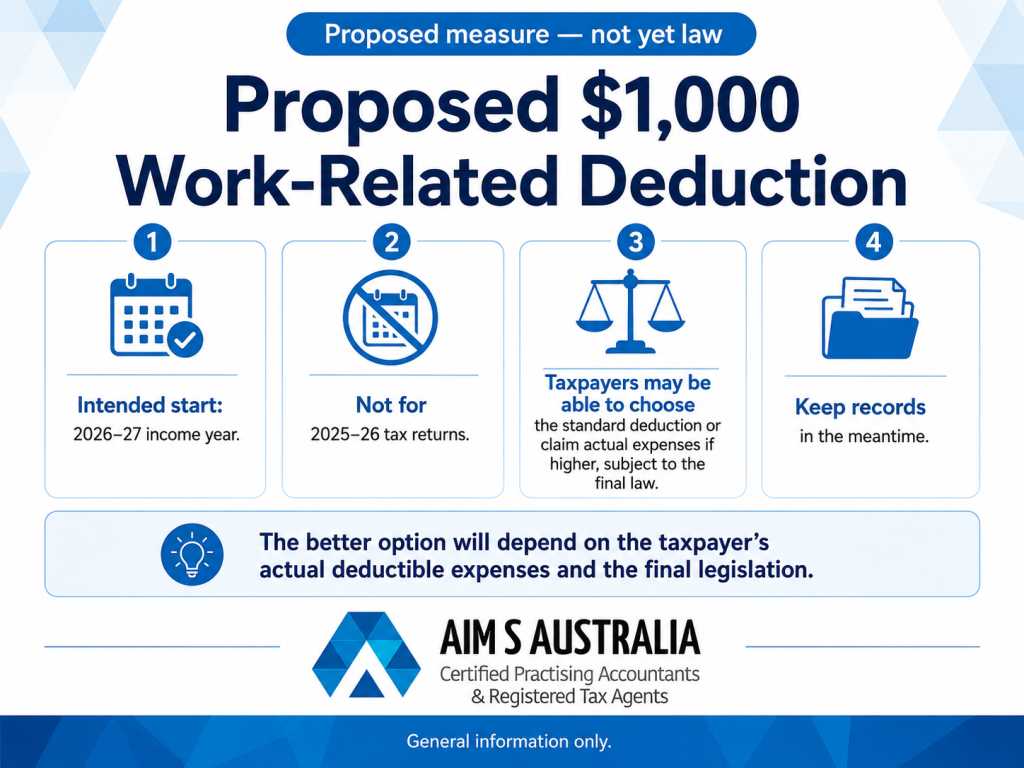

Proposed $1,000 Standard Work-Related Deduction

The Federal Government has announced a proposed standard deduction of up to $1,000 for eligible work-related expenses from the 2026–27 income year. At the time of writing, this measure is proposed and should not be treated as law until enacted. Taxpayers should continue to keep appropriate records and should not assume the deduction will apply to their circumstances.

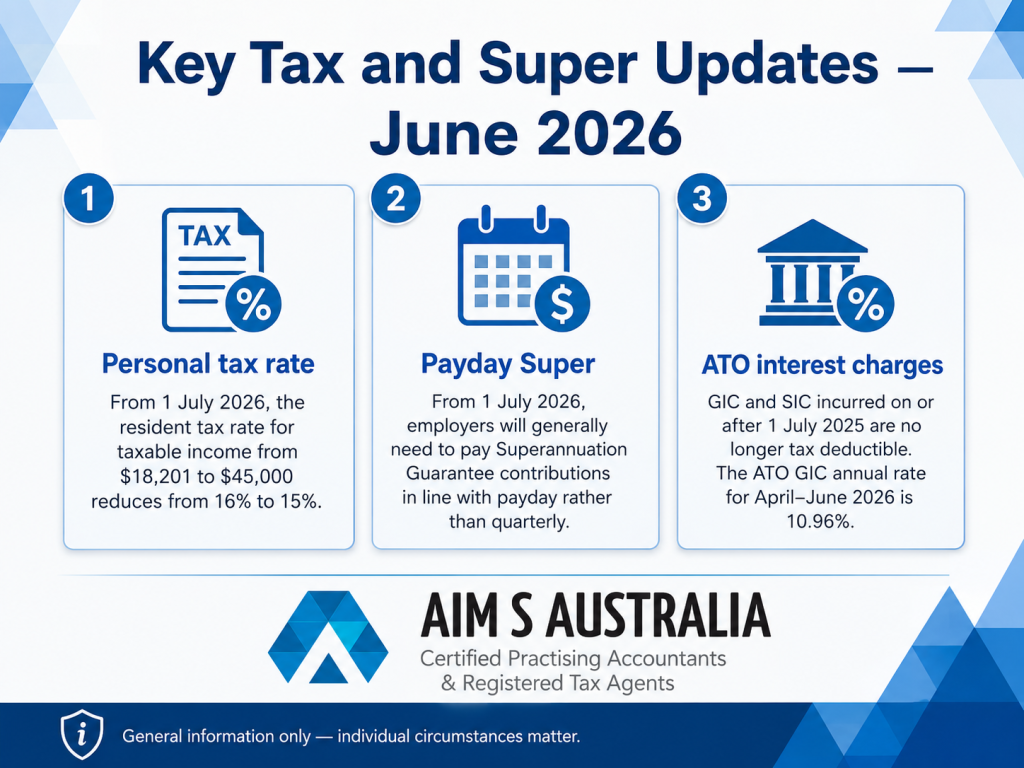

Personal Income Tax Rate Change from 1 July 2026

From 1 July 2026, the resident individual tax rate for the $18,201 to $45,000 taxable income bracket is scheduled to reduce from 16% to 15%. From 1 July 2027, it is scheduled to reduce further to 14%. These changes apply to Australian resident individual tax rates. Different rates may apply to foreign residents, working holiday makers, minors and other specific taxpayer categories.

Payday Super Starts from 1 July 2026

From 1 July 2026, employers will generally be required to pay superannuation guarantee contributions at the same time as salary and wages, rather than by the current quarterly due dates. Employers should review payroll systems, cash flow, super clearing house arrangements and employee onboarding processes before the change commences.

GIC and SIC Are No Longer Deductible from 1 July 2025

General interest charge and shortfall interest charge incurred on or after 1 July 2025 are no longer deductible. This means taxpayers carrying ATO debts may face a higher after-tax cost than in prior years. Interest incurred before 1 July 2025 may still be deductible, subject to the usual rules.

Recent FBT and Work-Related Deduction Developments

Employers and employees should also be aware of recent developments affecting fringe benefits tax and work-related deduction claims.

The Full Federal Court decision in Commissioner of Taxation v Toowoomba Regional Council is relevant to car parking fringe benefits. Employers providing employee parking should review whether nearby parking facilities may satisfy the definition of a commercial parking station for FBT purposes.

The Full Federal Court decision in Commissioner of Taxation v Hall [2026] FCAFC 43 is also relevant to employee work-from-home and travel deduction claims. The decision reinforces that merely performing work from home does not automatically make occupancy expenses deductible or make travel between home and a regular workplace deductible. The treatment will depend on the taxpayer’s facts, the nature of the expense and the relevant legal principles.

Employees should ensure work-related deduction claims are supported by both the law and the facts. COVID-era work-from-home arrangements should not be assumed to justify occupancy expenses.

EOFY Items to Review Before 30 June 2026

Superannuation Contributions

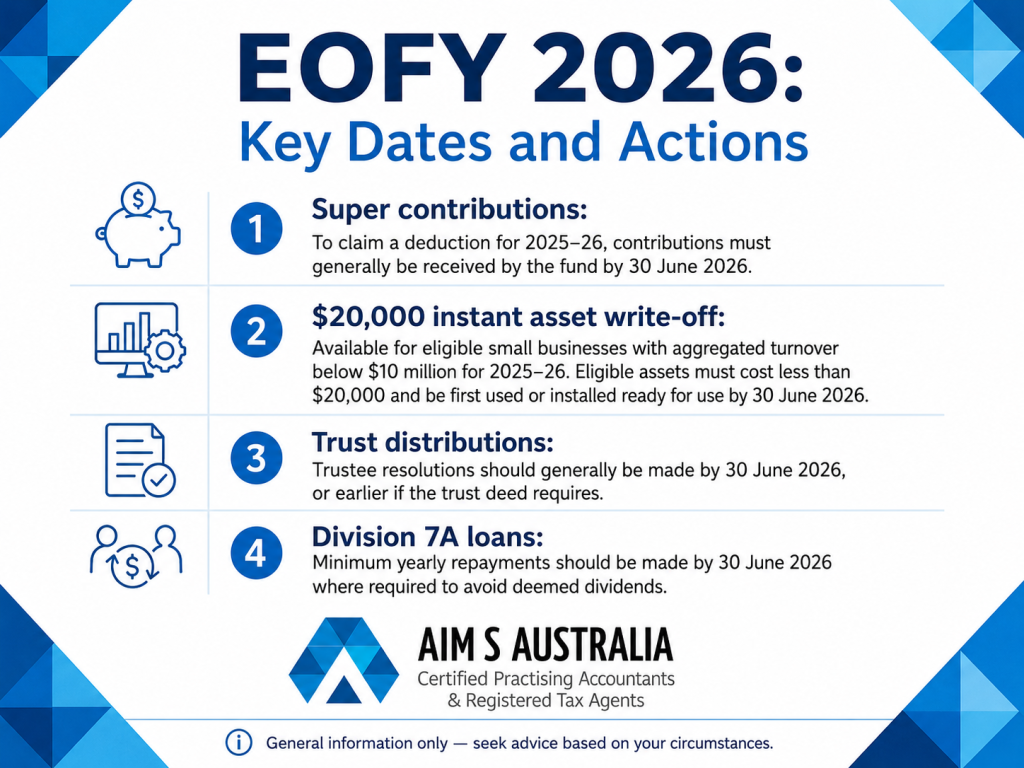

The concessional contributions cap for 2025-26 is $30,000. From 1 July 2026, the general concessional contributions cap increases to $32,500.

Some individuals may also be eligible to use unused concessional cap amounts from prior years if their total superannuation balance was below $500,000 at the previous 30 June.

Contribution timing is critical. Contributions must generally be received by the superannuation fund by 30 June to be deductible in the current financial year.

Taxpayers should check total concessional contributions across all funds, including employer contributions, salary sacrifice and personal deductible contributions, before making additional contributions.

Instant Asset Write-Off Considerations

Eligible small businesses should confirm the applicable instant asset write-off threshold for the relevant income year before acquiring depreciating assets. Timing, eligibility, business use, asset installation date and aggregated turnover requirements should be checked before relying on an immediate deduction.

Prepaid Expenses

Some prepaid expenses may be deductible upfront where the relevant prepayment rules are satisfied. Broadly, this may apply where the eligible service period is 12 months or less and ends by the end of the next income year.

The prepayment rules are technical and depend on the taxpayer, the expense, the service period and the surrounding facts.

Trust Distributions

Trustees should review the trust deed and prepare valid distribution resolutions before 30 June 2026 where required. The resolution should be consistent with the deed and should properly deal with any income streaming, capital gains, franked distributions, default beneficiaries, family trust election issues and unpaid present entitlements.

Division 7A Loans and Unpaid Present Entitlements

Private company groups should ensure minimum yearly repayments on Division 7A loans are made by 30 June where required. Failure to make minimum repayments can result in deemed unfranked dividends.

Trusts with corporate beneficiaries should also review unpaid present entitlement positions before year-end, as these arrangements may have Division 7A implications.

ATO Fuel Response and Temporary Payment Support

The ATO has outlined temporary support measures for eligible businesses affected by increased fuel costs. The ATO Fuel Response Payment Plan is available by application until 30 June 2026 for eligible taxpayers.

Support may include more flexible payment plan arrangements and, where the relevant conditions are satisfied, remission of General Interest Charge.

Separately, the heavy vehicle road user charge has been set to zero for the period 1 April 2026 to 30 June 2026, which may affect fuel tax credit calculations for eligible taxpayers.

Businesses experiencing cash-flow pressure should seek advice early and engage with the ATO before debts become unmanageable.

When Tax Matters Become More Complex

Taxpayers with more complex circumstances may need to consider lodgment status, residency, income source, CGT events, GST/BAS obligations, ATO debt and available records before lodging or amending returns.

AIMS Australia Tax Accountants assists individuals, expatriates, property investors, small businesses and business owners with Australian tax compliance and advisory matters, including overdue tax returns, expat and non-resident tax returns, Australian tax residency reviews, rental property tax schedules, foreign income reporting, BAS/GST compliance, ATO debt matters and CGT advice.

Final Comments

The end of the financial year is an important time to review tax positions, documentation, payroll compliance, superannuation timing and business cash flow.

However, several measures discussed above are fact-specific, and some remain subject to final legislative processes. Taxpayers should avoid making assumptions based on general announcements and should obtain professional advice before acting.

Disclaimer

This article is general information only and does not constitute tax, legal, financial or business advice. It has been prepared without considering any taxpayer’s specific facts, residency status, income profile, business structure, documentation, timing or applicable legislative requirements. Tax laws and administrative guidance can change. Taxpayers should obtain professional advice before acting or relying on this information. AIM S Australia Pty Ltd and the author accept no responsibility for loss arising from reliance on this general information without obtaining appropriate professional advice.